- Best Ever CRE

- Posts

- 📈 How NASA and defense towns fuel emerging multifamily markets

📈 How NASA and defense towns fuel emerging multifamily markets

Plus: A billion-dollar merger, bid intensity narrows, malls are so back, and much more.

Best Ever CRE Team

March 15, 2026

Together With

👋 Happy Sunday, Best Ever readers! An Australian startup is working on building “biological data centers” that are powered by living human brain cells. The future is weird.

In today’s newsletter, NASA elevates multifamily, a billion-dollar merger, bid intensity narrows, malls are so back, and much more.

Today’s edition is presented by Tribevest, the platform helping Sponsors and capital partners structure Fund of Funds and raise capital for private deals. Do people in your network ever ask you about investment opportunities? You might be closer to raising capital for deals than you think. 👉 Learn how through the Institute for Structured Capital

▶️ Join us Thursday, March 19, at 1 PM ET with private capital expert Marcin Drozdz in a free live webinar breaking down why founder control is the hidden ceiling on most raises, and the exact systems operators use to scale past it. Register now.

Let’s CRE!

🗞️ NO-FLUFF NEWS

CRE HEADLINES

🏦 Massive Merger: London-based Savills has agreed to acquire Eastdil Secured for more than $1.1 billion, combining platforms across 70 countries to become the No. 2 capital markets broker for deals of $100 million or larger.

⚡ Terminal Risk: Soaring oil and gas prices have elevated what one CRE consultancy is calling "terminal risk" for buildings tethered to fossil fuels, with European CRE transactions falling 9% YoY in Q4 while investors in energy-efficient assets are projected to see shortened payback periods.

📊 Bid Gap: Investor bidding intensity across multifamily, industrial, retail, and office has narrowed to its smallest spread in more than three years, according to JLL's Global Bid Intensity Index, as pricing alignment between buyers and sellers signals a return to normalized market conditions.

🛍️ Mall Rats: Gen Z shoppers have emerged as a bright spot for mall recovery, with 18-to-24-year-olds buying 62% of general merchandise purchases in stores last year — outpacing older generations — as retailers like Pacsun and Edikted expand their physical footprints to meet demand.

🏪 Quiet Return: U.S. banks have cautiously re-entered retail lending after years of contraction, with 11 of 18 major banks reporting higher retail loan balances in 2025 as grocery-anchored centers post solid fundamentals and fewer credit surprises.

🏆 TOP STORY

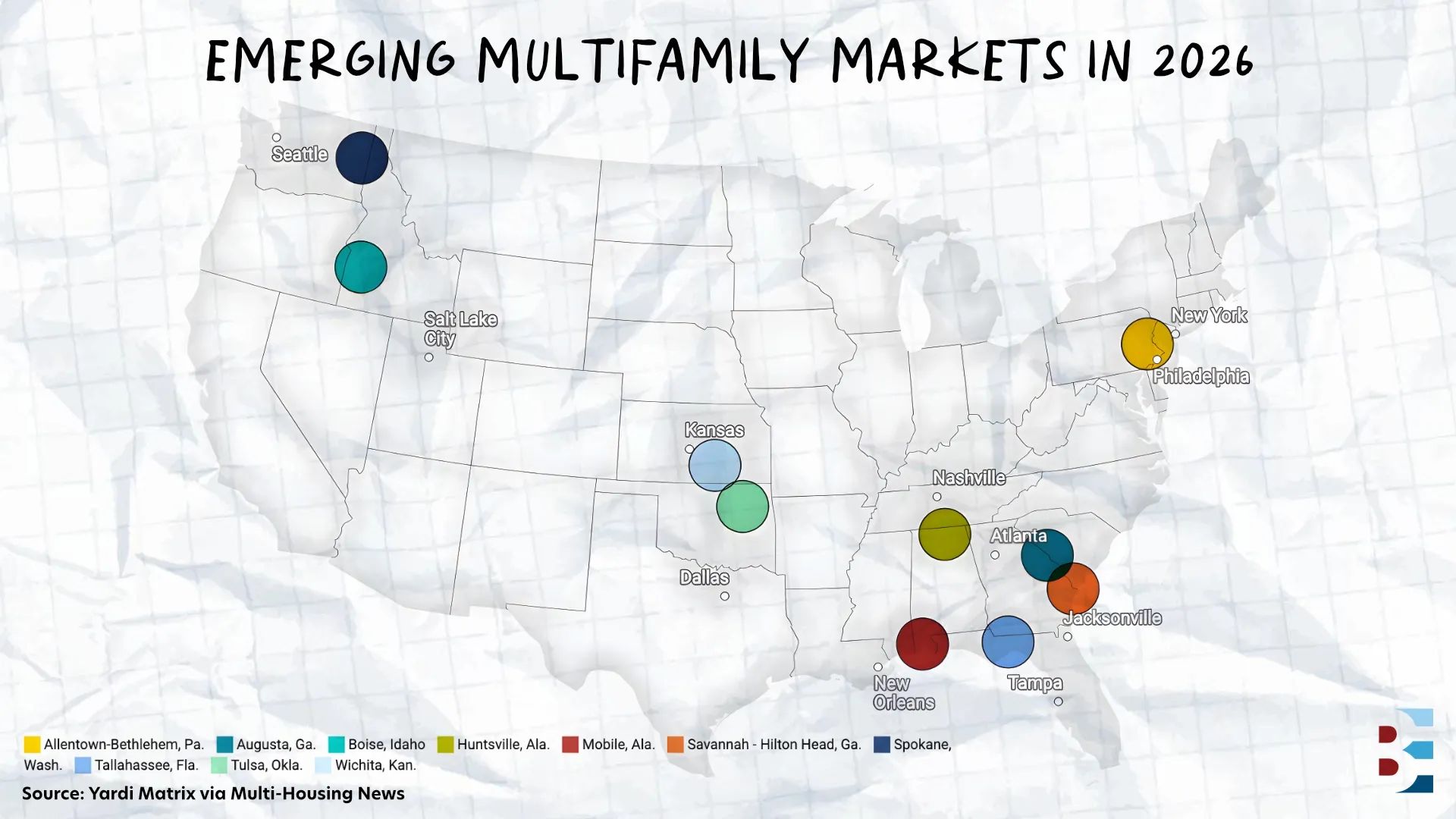

NASA, DEFENSE TOWNS FUEL TOP EMERGING MARKETS

NASA doesn't show up in most multifamily pitch decks. Neither does Fort Eisenhower, or the Port of Savannah, or Wichita's aerospace manufacturing corridor. But this year's ranking of top emerging multifamily markets suggests that defense installations, logistics hubs, and university anchors are doing more to sustain rental demand in mid-sized metros than the relocation booms that defined the post-2020 Sun Belt surge.

Five of the 10 markets featured sit in the Southeast, but the throughline isn't warm weather or low taxes, it's durable employers. Defense installations underpin at least half the ranking, most visibly in Huntsville and Augusta, while port logistics anchor Savannah–Hilton Head and Mobile, and university employment stabilizes Tallahassee.

Nationally, 2026 is projected to bring approximately 469,000 multifamily deliveries and rent growth of around 1.2%, and the markets below are absorbing new supply while drawing consistent capital.

Huntsville, AL: Anchored by Redstone Arsenal, NASA's Marshall Space Flight Center, and a dense network of defense contractors, Huntsville recorded 4,008 deliveries in 2025 with 4,848 units still under construction, the second-largest active pipeline in this group. Per-unit price growth hit 28.4% YoY. The caveat: occupancy sat at 92.3%, the lowest among these markets and down 120 bps YoY, as new supply works through the system.

Tallahassee, FL: Leaning on Florida State University and state government employment, Tallahassee posted 134.1% YoY per-unit price appreciation, the fastest on the list.

Augusta, GA: Fort Eisenhower's cyber and defense activity drove 1.3% YoY employment growth, second-fastest in the group, and $315 million in sales volume.

Tulsa, OK: The fastest employment growth of any market at 1.4% YoY, with an average price per unit of $92,650, the most accessible entry point on the list.

Mobile, AL: The strongest occupancy improvement at 60 bps YoY, bucking the national 30-bps decline, anchored by a port economy and aerospace and shipbuilding operations.

Allentown–Bethlehem, PA: The tightest occupancy on the list at 96.7%, up 40 bps YoY, driven by its position in the Northeast's distribution corridor.

Wichita, KS: Just 392 units (1% of stock) delivered in 2025, yet per-unit price growth hit 117.2% YoY, third-fastest on the list.

Boise, ID: The only market priced above the national average at $226,380 per unit, with the second-highest delivery rate at 8.1% of stock and 2,969 units under construction.

Savannah–Hilton Head, GA: Led all 10 markets in both sales volume at $436 million and deliveries at 5,088 units, with 6,050 units still under construction, the largest active pipeline in the group.

Spokane, WA: Occupancy held at 94.6%, third-highest in the group, with 4,423 units under construction, the third-largest pipeline on the list.

Nine of the 10 markets are priced below the national average of $206,100 per unit. That affordability gap, alongside durable economic anchors, is what's drawing capital to this tier and separating these metros from markets still fighting for the same institutional dollars.

THE BOTTOM LINE

The mid-sized market thesis for 2026 isn't built on speculation. Savannah, Augusta, and Mobile each ranked in the top three for investment volume among this peer group. Allentown's occupancy tightness points to a supply-demand balance that most larger markets can't match. With financing conditions expected to remain comparatively active and per-unit pricing sitting below the national average across nearly the entire list, these markets are where supply and fundamentals are moving in the same direction.

🤝 TOGETHER WITH TRIBEVEST

FROM CONNECTOR TO CAPITAL PARTNER

Some of the most successful capital raisers didn’t start as full-time fund managers.

They started as connectors — people who had relationships with investors and access to strong deals.

The challenge is turning those introductions into a structured capital raising project that investors trust and Sponsors welcome.

That’s why Tribevest created the Institute for Structured Capital (ISC).

ISC teaches aspiring capital partners how to:

Work with Sponsors through Fund of Funds

Structure a compliant capital raise

Organize investor interest professionally

Build a repeatable capital raising process

If you’ve ever thought about bringing your investor network into a deal, ISC is where the process begins.

💰 CRE TRENDS

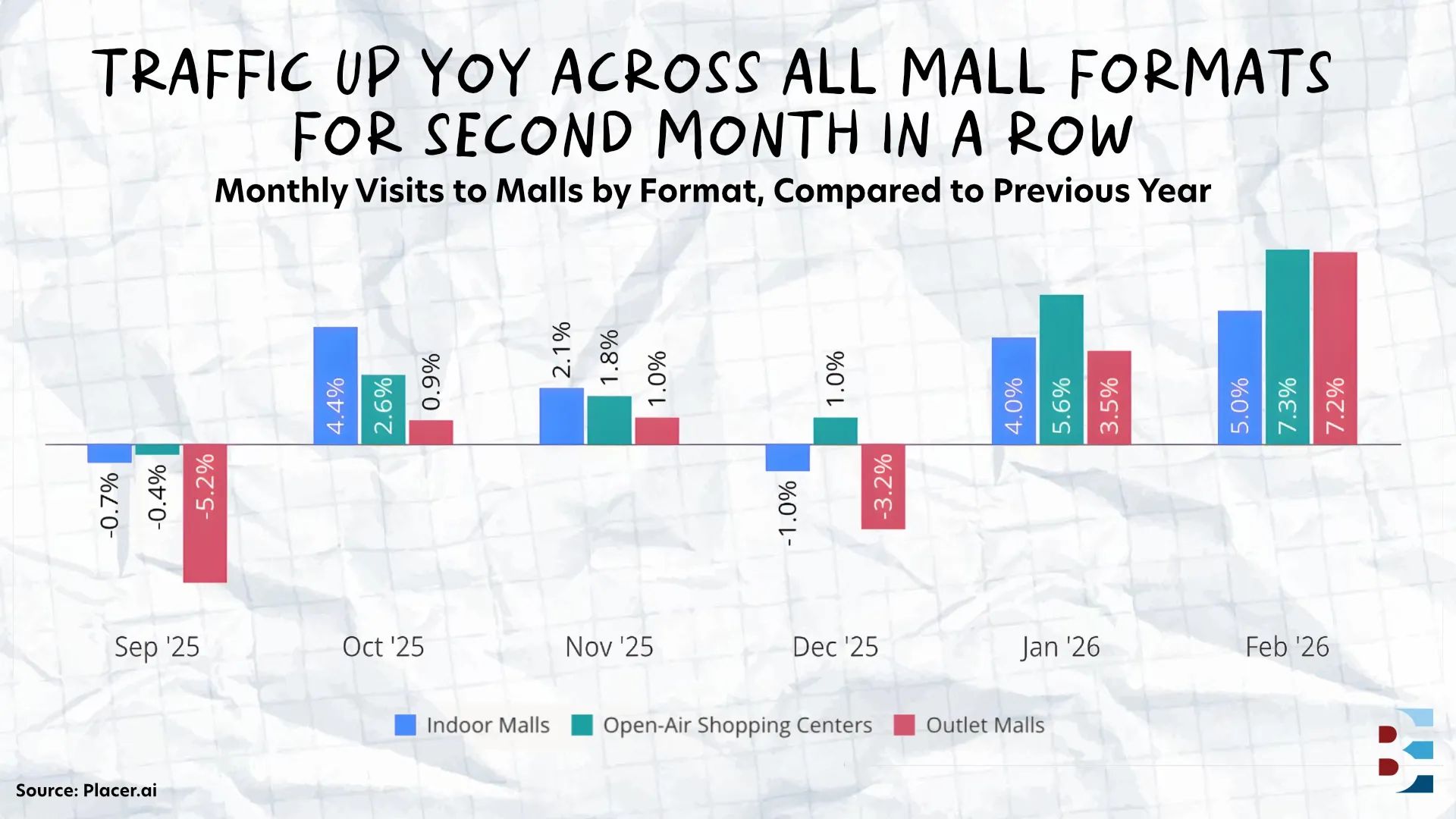

DON’T LOOK NOW, BUT MALLS ARE SO BACK

Shopping centers extended their growth streak in February, with all three formats — indoor malls, open-air centers, and outlet malls — posting YoY visit gains, according to the Placer.ai Mall Index.

Open-Air Still Leads: Open-air centers topped the category with 7.3% YoY visit growth in February. Outlet malls followed at 7.2% — a notable jump from 3.5% YoY in January — suggesting the format is regaining momentum after a recent lull.

Outlets Win Peak Hours: When isolating peak hours (11 a.m. to 8 p.m.), outlet malls led all formats in YoY visit growth across every daypart. Evening gains were strongest across the board, with outlets posting the most significant increase during that window.

The Experience Play: The evening momentum may signal a broader repositioning. Some outlet centers are adding dining and experiential offerings — craft beer concepts, new restaurant debuts — to encourage longer, more social visits rather than purely transactional trips.

Off-price retailers and resale channels have pressured outlet traffic in recent years by siphoning bargain-focused demand. The February data suggests outlets that can compete on experience, not just price, may be better positioned heading into the rest of 2026.

▶️ YOU’RE INVITED

DON’T LET FOUNDER CONTROL CAP YOUR CAPITAL RAISE

The operators scaling past $50M aren't raising harder. They're raising smarter.

Over $3 billion in transactions. Nine figures raised. More than 1,000 operators advised. Marcin Drozdz has seen exactly where capital raises break down — and it's rarely the market.

In most cases, it's the founder.

🗓️ Join us alongside Marcin on Thursday, March 19 at 1PM ET for a free live webinar where he shares the exact infrastructure shifts that allow serious operators to scale from $5M to $50M without their constant presence in every investor conversation.

You'll walk away with:

The real reason founder control caps your raise velocity

How to keep capital moving without routing everything through you

The systems that make larger raises repeatable and scalable

🎙️ THE BEST EVER CRE SHOW

NINE DEALS, EIGHT LENDERS, AND ONE BUYING THESIS

Cap rates in Tucson, AZ, are at their highest level in 13 years, and Gary Lipsky is buying.

Why are we talking Tucson? Because Lipsky, a multifamily operator, joined Pascal Wagner on the Best Ever CRE Show this week to break down his latest 300-unit Tucson acquisition, why he sees 2026 as a generational buying window, and the behind-the-scenes reality of managing nine active deals through a difficult rate environment.

Lipsky's newest deal — a 300-unit property at 110 Adora in Tucson — is his 12th acquisition in that market, and he says it checks all four boxes every deal must hit: cash flow, appreciation, depreciation, and capital preservation. The math, he says, is simple: Where investors were buying at a 4% cap rate in 2021–2022, today's deals are clearing 6%+, meaning more income per dollar spent.

The Opportunity Thesis: Lipsky's case for buying now comes down to timing. Deal volume in Tucson cratered from roughly 27 transactions of 100+ units in 2022 to approximately three the following year, and sellers who bought at peak valuations still won't move. That reluctance — combined with rate-driven fear keeping capital on the sidelines — has created a window. His view is that interest rates will come down, values will follow upward, and the investors waiting for certainty will have missed it. "People will be looking back in a year or two and being regretful that they didn't buy in 2026," Lipsky says.

Lender Dynamics: Across nine active deals with eight different lenders, Lipsky describes a wide range of experiences. Some have worked cooperatively — dropping rates, extending loan terms, buying operators time to wait out the market. Others have withheld reserves on performing assets. Where lenders won't budge, Lipsky has paid down loans to unlock extensions, explored capital calls, and structured deals that let existing investors participate in paydowns to avoid forced outcomes.

Asset Management Discipline: When occupancy starts slipping, the cost to recover is steep — and Lipsky argues most operators don't see it coming because they stopped paying attention. His team adjusts rents and concessions weekly on a per-unit basis, tracks every unit individually, and maintains daily contact with property managers across the portfolio.

The math on deferred maintenance is unforgiving. Lipsky has watched operators let occupancy slide from 90% to 60% by cutting corners — and the cost to recover, he says, is far greater than whatever they thought they were saving. His team puts money into every property, every cycle, no exceptions. In a market where lenders are watching and investors are waiting, that discipline isn't a virtue — it's a survival strategy.

✅ BEST EVER RECOMMENDATIONS

A FREE GUIDE TO SMARTER MULTIFAMILY INVESTING

Most multifamily investors don't fail because of bad luck — they fail because of questions they didn't know to ask. REEP Equity's free white paper, Navigating Multifamily Investing: Steering Success & Avoiding Common Pitfalls, breaks down the missteps that quietly derail deals and how to avoid them.

From location analysis and financial due diligence to finding the right partners and spotting growth potential, this is a practical resource for anyone looking to invest with more confidence.

🙏 Thanks for reading!

Stay in the loop with us! If you received this newsletter from someone else, subscribe here. You can also find us on LinkedIn, Instagram, and YouTube.

Have a Best Ever day!

— Joe Fairless