- Best Ever CRE

- Posts

- 📍 Where every renter report points in 2026

📍 Where every renter report points in 2026

Plus: Self storage surges, the stealth manufacturing boom, Hilton enters flex living, secondary markets outperform, and much more.

Best Ever CRE Team

April 23, 2026

Together With

👋 Hello, Best Ever readers!

In today’s newsletter, renter reports play favorites, self storage surges, Hilton enters flex living, secondary markets outperform, and much more.

Today’s edition is presented by Equity Institutional Services. Your investors have IRA capital — most sponsors just don't know how to access it without slowing down their raise. Equity Institutional Services gives you the custody infrastructure, dedicated support, and sponsor-friendly tools to make self-directed IRA participation a standard part of every offering. Download the free Capital Raise Guide.

🦙 TODAY, Property Llama Co-Founders Chris Lopez and Richard McGirr are walking through three private credit strategies targeting 16–20%+ annual cash flow — backed by real assets, structured for downside protection, and designed to work together. Live Q&A included, and spots are almost gone. Save your seat →

Let’s CRE!

🗞️ NO-FLUFF NEWS

CRE HEADLINES

📉 Sentiment Shock: The CRE Finance Council (CREFC) Board of Governors Sentiment Index has dropped 20.2% QoQ in Q1 2026 — erasing three quarters of gains — as all nine tracked indicators deteriorated, with rates, liquidity, and macro outlook hit hardest.

🏭 Stealth Factory Boom: U.S. manufacturing output has risen 2.3% since January 2025 even as 100,000 factory jobs disappeared, driven by AI-linked demand — semiconductors, aerospace, and data center infrastructure.

🏘️ Secondary Rent Winners: Twelve secondary markets have logged rent growth above 3% YoY through March 2026 — Urban Honolulu led at 7.1%, Champaign-Urbana at 5.8% — while the U.S. overall averaged a 0.5% decline.

🏨 Apart-Hotel Arms Race: Hilton's new Apartment Collection brand has opened its first two properties via a Placemakr partnership, targeting up to 3,000 units as Marriott and Wyndham chase the same flex-living category.

🏗️ Storage Surge: Self storage supply will hit 55.4 M SF nationally in 2026 — a 2.6% inventory increase — with FL alone delivering 10.3 M SF and 14 of the top 20 delivery metros located in the South.

🏆 TOP STORY

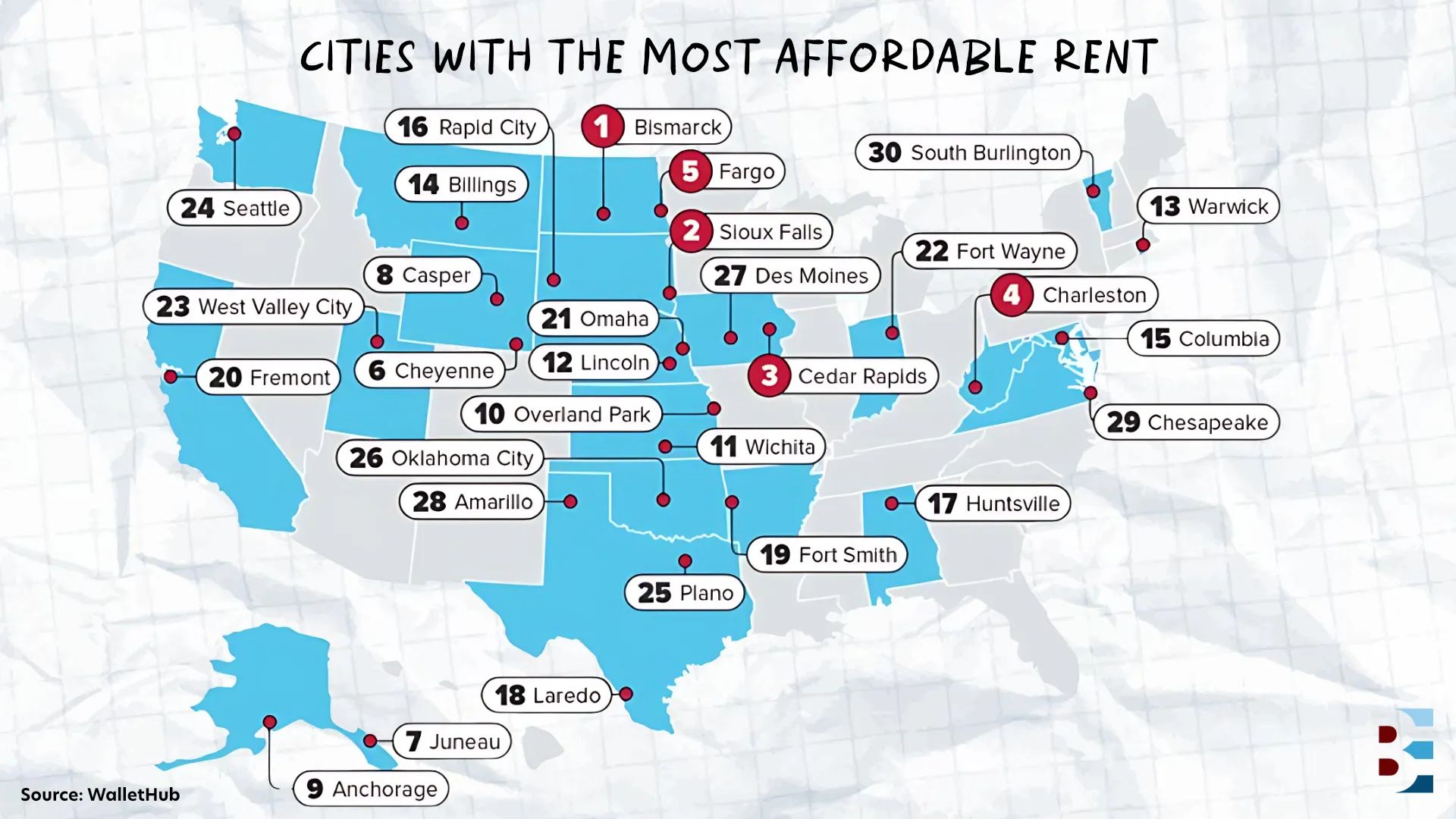

WHERE EVERY RENTER REPORT POINTS IN 2026

In Sunday's newsletter, we broke down ConsumerAffairs' annual renter-friendliness rankings, but it’s part of a larger market convergence story.

Over the past few weeks, Arbor Realty Trust, Redfin, Glassdoor, WalletHub, Apartment List, and Realtor.com each dropped national studies breaking down renter trends and how demographics are shifting market to market. Each is measuring something different: investor opportunity, rent-to-income ratios, workforce relocation patterns, behavioral search data, and demographic segmentation.

We combed through the data to determine which markets keep surfacing near the top regardless of methodology, and a handful of key markets shone consistently across the reports.

🏭 Indianapolis

Thirty consecutive months of above-national rent growth. A 7.9-percentage-point YoY gain in rental occupancy — the largest among the 75 biggest U.S. markets. A diversified employment base anchored by logistics, healthcare, and life sciences. Arbor and Chandan Economics rank Indianapolis No. 1 among the 50 largest multifamily markets in their Spring 2026 Opportunity Matrix, and the underlying numbers explain why: vacancy has tightened to some of the lowest levels among large markets nationally, while WalletHub's rent-to-income data puts the city at 20.95% — well within the range where renter households retain real financial flexibility.

🔬 Raleigh/Durham

Arbor's second-ranked market overall, and one of the most in-demand destinations on Apartment List's 2026 migration report, with over 60% of Durham's inbound searches originating from out-of-towners — the third-highest share nationally. A technology and advanced manufacturing employment base continues absorbing new supply, and Cushman & Wakefield's Q1 retail data shows Raleigh/Durham vacancy at 3.4%, among the tightest in the country — a useful signal of how firmly rooted the consumer base is.

🎯 Nashville

Absorption well above historical norms. Family renters — the largest and most stable renter cohort nationally at 44% of all renter households, per Realtor.com's renter segmentation report — are choosing Nashville at an outsized rate. Arbor ranks it fourth on its composite matrix, and ConsumerAffairs places Tennessee in the upper tier for rental availability. New supply has been delivering, but demand has kept pace.

🏔️ Salt Lake City

Arbor's third-ranked market, with solid job growth, low unemployment, and above-average absorption. ConsumerAffairs places Utah fifth best for renters statewide, citing new construction availability and a vacancy rate that gives renters real options. Apartment List tracks consistent inbound migration from higher-cost Western metros — particularly the Bay Area and Sacramento corridor — with Salt Lake City among the primary receiving markets.

🌾 The Midwest

No single city sweeps every report, but no region comes close to matching the Midwest's consistency. WalletHub's five most affordable cities are all Upper Midwest and Great Plains metros, with rent-to-income ratios between 15% and 17%. Arbor places Milwaukee fifth and Chicago eighth nationally, and Yardi Matrix shows Chicago leading major markets in annual rent growth at 3.6% YoY. ConsumerAffairs ranks North Dakota No. 1 for the third consecutive year, with renters spending just 23.7% of income on housing.

What connects these markets isn't a breakout metric. It's the absence of the structural problems — overbuilding, wage-rent mismatches, supply pipelines that outran demand — that made other markets fragile going into 2026.

THE BOTTOM LINE

These markets score well across six independent methodologies because they've earned it. For operators and investors, that consistency is the signal: lower lease-up risk, a stable renter base, and fundamentals that hold up when the macro environment doesn't cooperate.

🤝 TOGETHER WITH EQUITY INSTITUTIONAL SERVICES

UNLOCK A HIDDEN SOURCE OF CAPITAL

Many capital raisers overlook one of the largest pools of investable assets: IRAs. With trillions available,* more investors are actively looking for opportunities like yours.

Equity Trust makes it easy to get investors set up, funded, and into your raise quickly and without unnecessary friction.

From day one, you’ll have a clear, transparent process and a responsive team by your side. No guesswork. No delays. Just straightforward support and consistent communication every step of the way.

Raise capital more efficiently and get back to focusing on your next opportunity.

👇 Download their Free Capital Raise Guide to learn more.

💰 CRE BY THE NUMBERS

RETAIL RENTS RISE, INDUSTRIAL VACANCY DIPS, AND MORE

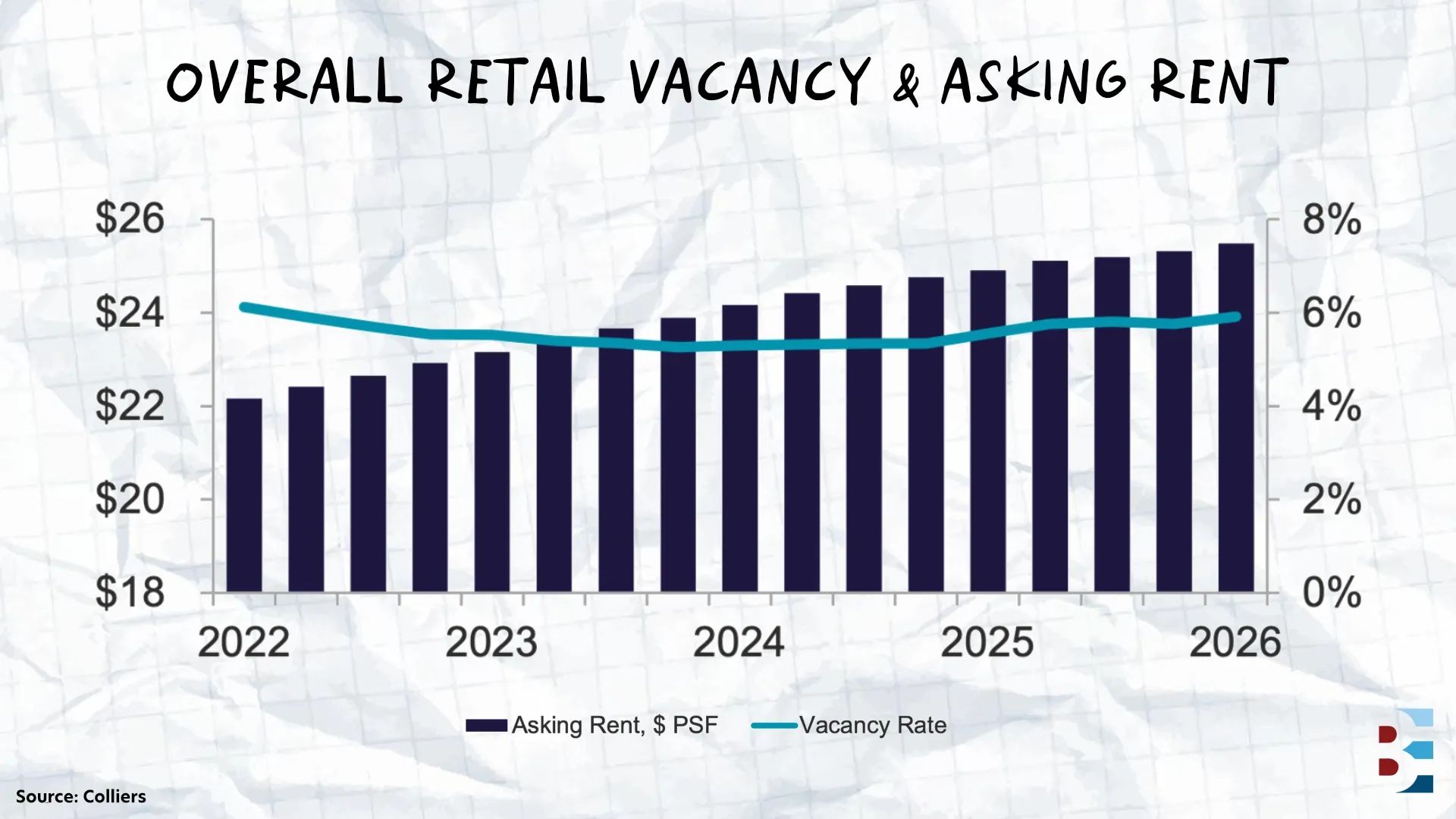

🛍️ $25.48 PSF

Retail asking rents rose 2.3% YoY to $25.48 PSF nationally in Q1, even as shopping center absorption came in at -4.6M SF — the third consecutive Q1 on negative footing. With only 2.1M SF delivered and the active pipeline representing less than 0.3% of existing inventory, supply constraints continue to support rent growth despite softening occupancy.

🏦 $1.19 Billion

Bank of America's nonperforming CRE loans fell 44% YoY to $1.19 billion in Q1, leading a broad improvement across major lenders. Wells Fargo's nonperformers dropped to $3.78 billion and PNC's fell 26% to $630 million, as credit quality held firm despite elevated inflation and global uncertainty.

🏭 174M SF

Industrial leasing hit 174M SF in Q1 — the strongest first quarter since 2022 — as vacancy dipped 10 bps from its late-2025 peak to 7%. Just 54M SF of new supply came online, the lowest volume since mid-2017, and net absorption came in at 40M SF positive as demand outpaced space givebacks.

📝 BEST EVER RESOURCES

FUND OF FUNDS DEEP DIVE FREE DOWNLOAD

There is a structural advantage in private markets that very few investors have been introduced to or understand.

AAA Storage Investments built a program that turns experienced investors into capital aggregators, and the math is worth paying attention to. The same deal. The same assets. A capital aggregator raising $1M can increase their returns dramatically and generate a 42% IRR versus 20% as a direct investor.

This is a strategy. A real growth opportunity with a built-in compliant structure and a back office that handles the heavy lifting. The full breakdown covers the economics, who it is built for, and what it takes to get started.

🏘️ DEAL OF THE WEEK

79-LOT MHP TARGETS 3.0X MULTIPLE THROUGH REFI-AND-HOLD STRATEGY

Cory Harelson and the team at Freedom Investing Group acquired this 79-lot manufactured home community in Nicholasville, KY, for $2.4 million in May 2024 — and are already ahead of schedule on distributions while executing a value-add plan targeting a 20% IRR and 3.0x equity multiple over 10 years.

Here's how they're doing it 👇

🏢 Property details: This 79-lot manufactured home community is located in Nicholasville, KY. The property was acquired in May 2024 for $2.4 million. With 24 vacant lots and below-market rents at acquisition, the team identified significant upside through lot fill-up and rent increases.

💸 Finances: The team raised $1.8 million in equity capital. Debt was structured at 65% LTV and 47% LTC with a 10-year fixed rate that resets at year five.

💼 Business plan: The team is investing $400,000 in capital improvements — road repairs, skirting and painting homes, fencing, and signage — to bring curb appeal in line with the surrounding high-value residential neighborhood. The value-add strategy focuses on two levers: filling the 24 vacant lots with a mix of new and used homes using $300,000 in recycled home-purchase capital, and bringing lot rents up to market rates to drive NOI growth. The target exit is a cash-out refinance somewhere between years three and seven, returning investor capital while retaining the asset for long-term cash flow — a structure that targets an infinite cash-on-cash return for investors post-refi.

🍾 Results: The deal is active and ahead of schedule on distributions and income. Targets over a 10-year hold:

20% IRR

3.0x equity multiple

Infinite cash-on-cash return (post cash-out refinance)

💪 Biggest challenge: "The previous owner had a toxic relationship with the county. The county tried to stop them from filling vacancies, and they had to sue the county to be allowed to install new homes. We took the approach of working with the county, listening to their concerns, and addressing any issues they saw. We now have a much better relationship with them. Additionally, when we took over the property, it had a lot of deferred maintenance. We fully repaved the roads and did over $100,000 in tree work to address overgrowth that hadn't been dealt with in probably decades."

🎉 Bonus win: The property came with a strip of vacant land at the rear that contributed nothing to underwriting. A housing development under construction directly behind the property created an opportunity — the team sold the land to the developer, generating $70,000 in additional investor returns that weren't in the original model.

👉 If you have a deal you'd like to share with us, please submit it here.

🎙️ THE BEST EVER CRE SHOW

THE RATIO METRICS THAT KEEP FUNNELS HONEST

Lead generation looks like a growth strategy until the leads stop converting. At that point, it's just an expensive spreadsheet.

Unlimited Capital host Richard McGirr took to the Best Ever CRE Show this week to discuss why volume targets without quality controls don't just fail — they actively obscure what's going wrong in your capital raising funnel.

The Core Framework: Every absolute metric needs a paired ratio metric. Lead volume without a lead-to-call rate, an accredited investor ratio, or a media cost of capital benchmark just measures activity. McGirr runs his operation against floors and targets on each — channels that drop below the floor get audited and shut down.

The Speed-to-Lead Factor: Waiting until the next day to call a webinar attendee produces a 90–95% drop in contact productivity compared to calling same day. McGirr's rule: every paid webinar attendee gets a call before the day ends. The window is that short.

What Good Traffic Actually Costs: McGirr targets a media cost of capital between 1–2%, meaning for every dollar spent on lead generation, he expects to raise $50 to $100 in LP capital. Channels that can't clear that threshold within 90 days get cut.

The operators building durable capital raising businesses aren't the ones with the biggest lists. They're the ones who know exactly which leads are worth chasing — and which channels are burning money.

🙏 Thanks for reading!

Stay in the loop with us! If you received this newsletter from someone else, subscribe here. You can also find us on LinkedIn, Instagram, and YouTube.

Have a Best Ever day!

— Joe Fairless