- Best Ever CRE

- Posts

- 🗺️ Why some markets are running out of renters

🗺️ Why some markets are running out of renters

Plus: Underwriting gets sloppy, utility costs fall, Exxon relocates, and much more.

Best Ever CRE Team

March 12, 2026

👋 Hello, Best Ever readers!

In today’s newsletter, America gets older, underwriting gets sloppy, utility costs fall, Exxon relocates, and much more.

📩 Is founder control quietly stalling your capital raise? On March 19 at 1 PM ET, private capital expert Marcin Drozdz is hosting a free live webinar breaking down why your constant presence in every investor conversation may be the biggest bottleneck in your raise — and how to fix it. Save your spot.

Let’s CRE!

🗞️ NO-FLUFF NEWS

CRE HEADLINES

💸 Bad Underwriting: Pimco is warning of a reckoning across the $1.8 trillion private credit market, citing years of sloppy underwriting as the root cause. Defaults are projected to hit mid-single digits, with investor returns expected to drop from around 10% to as low as 6%.

⚠️ Distress Lingers: CRE special servicing rates hit 11.1% in February — the second-highest level since the Global Financial Crisis — with office delinquencies approaching double digits and overall distress expected to hold between 11% and 12.5% through mid-2026.

🏙️ ATL Rising: Atlanta's multifamily market is forecast to post 4.1% rent growth in 2026 — second highest nationally — as vacancy tightens 50 bps to 5.2% and new supply drops by 8,400 units compared to last year.

🏠 BTR Backlash: More than 42 industry groups, including the Mortgage Bankers Association and the National Apartment Association, are urging the Senate to strip a provision from a housing bill that would require large build-to-rent developers to sell communities within seven years of construction.

🧖 Getting Well: Social wellness clubs are emerging as a booming business model, with Bathhouse projecting $120 million in run-rate revenue from two New York locations as operators tap growing consumer demand for alcohol-free, community-centered social spaces.

🏆 TOP STORY

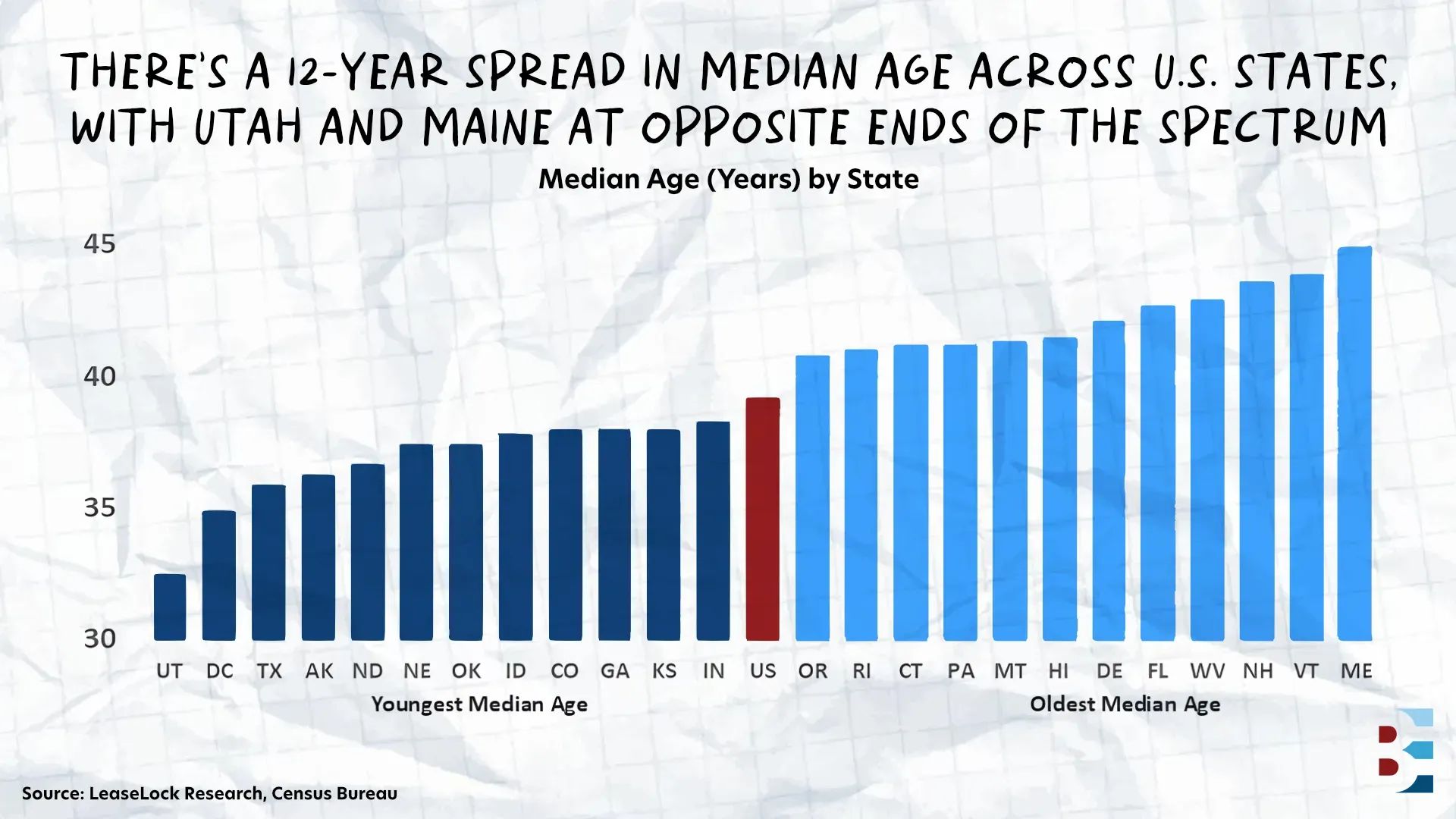

THE AGE CURVE IS RESHAPING MULTIFAMILY UNDERWRITING

The U.S. median age crossed 39 this year, and it has been climbing steadily since 1980. For most people, that's a demographic footnote. For multifamily investors, it's a revenue story hiding in plain sight.

The gap between the nation's youngest and oldest states now spans more than a decade. Utah's median age sits at 32.5; Maine's is nearly 45. That spread matters because young singles living alone still account for an outsized share of the renter base — making state-level age a rough but useful proxy for household formation depth and, by extension, demand for both new and existing apartment stock.

Younger markets — Utah, Texas, Colorado, and Georgia among them — combine economic momentum with deep renter pipelines. Absorption stays strong, lease-up periods are shorter, and new-lease pricing has more room to run.

Older markets across New England and the Mid-Atlantic tell a different story: the renter pool replenishes more slowly, which can leave new supply more exposed and mute turnover-driven rent growth.

The counterintuitive piece is what older renter cohorts do for revenue stability. Residents move less frequently, and that stickiness compounds. Renewal lease rent growth is running near 4% nationally — roughly four times the approximately 1% growth on new move-in leases. Operators in renewal-heavy portfolios also sidestep the roughly $3,872 in per-unit turnover costs that come with every departing resident.

Retention Holds: RealPage data shows lease renewal conversion hit 55.1% nationally through mid-2025, up roughly 2% YoY — a record for many operators.

Operations Shift Accordingly: Younger markets reward dynamic pricing and amenity-driven differentiation. Older markets reward resident retention programs and measured renewal pricing that maximizes lifetime resident value.

The Underwriting Signal: Median age points investors toward where operational emphasis should lie and how to calibrate the trade-off between top-line demand growth and lower-volatility, renewal-driven income.

THE BOTTOM LINE

Younger states offer velocity and scale. Older-renter markets can deliver something closer to an annuity — steadier cash flows, lower frictional costs, and renewal pricing that outpaces new-lease growth. As underwriting grows more competitive, age distribution may become a more explicit input in how investors size both risk and opportunity.

📩 YOU’RE INVITED

HOW TO BUILD SYSTEMS THAT SCALE BEYOND YOU

Is founder control quietly killing your capital raise?

If your raises feel slower and harder to close, the market isn't the problem — you are. When every investor touchpoint runs through you, capital stalls.

📅 Join private capital expert Marcin Drozdz on Thursday, March 19, at 1 PM ET for a free live webinar where he breaks down exactly how to fix it.

You'll walk away knowing:

Why founder-dependent communication caps your raise velocity

How to keep capital moving without routing everything through you

The systems serious operators use to scale from $5M to $50M

Marcin has raised nine figures in private capital, consulted 1,000+ operators, and participated in over $3 billion in transactions. He knows what's breaking your raise — and how to rebuild it.

Can’t make the live event? Register anyway, and we’ll send you the replay.

💰 CRE BY THE NUMBERS

UTILITY COSTS, EXXON, ABORTION STATES, AND MORE

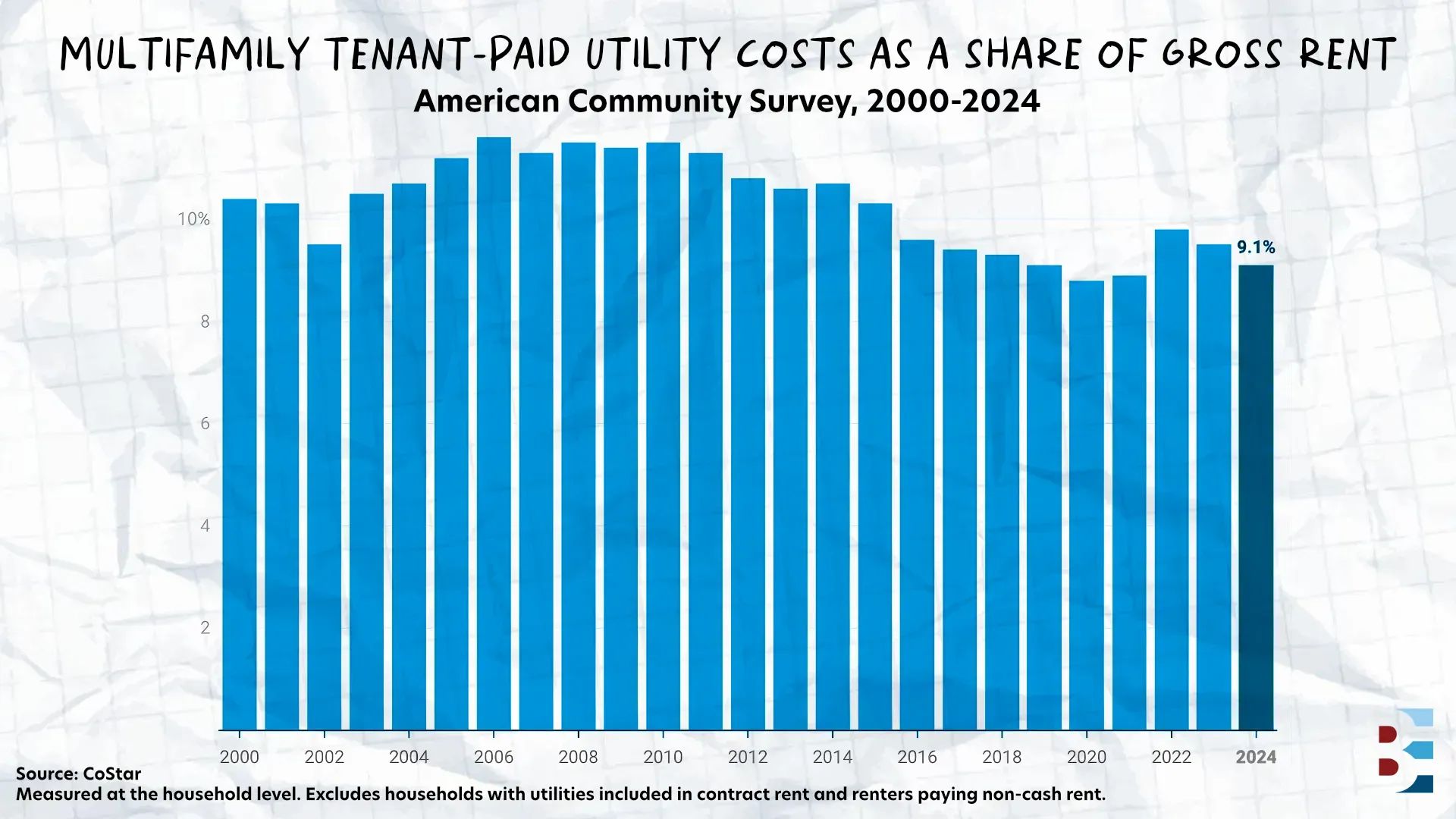

📉 8.8%

Multifamily utility costs have fallen from as much as 11.6% of gross rent in 2006 to 8.8% by 2020, according to Chandan Economics, driven by the U.S. shale boom, rising rents, more energy-efficient construction, and Sun Belt migration — a structural shift industry observers expect to hold.

🏢 86%

Office occupancy reached 86% in Q4 2025 — its second consecutive quarterly increase — as net absorption approached equilibrium for the first time in years, according to CoStar data. Retail held at 95.7%, while industrial and apartment sectors stabilized at 92.6% and 91.5%, respectively.

🤠 1882

Exxon Mobil plans to redomicile from New Jersey — where it has been incorporated since 1882 — to Texas, joining Tesla, Coinbase, and Chevron in a broader corporate migration to the Lone Star State driven by business-friendly courts and tightening shareholder lawsuit protections.

🏨 7.6%

The Baird Hotel Stock Index is up 7.6% YTD through February — outpacing the S&P 500's 0.5% gain — as better-than-expected RevPAR growth drove a third consecutive monthly increase and lifted investor sentiment across both hotel brands and REITs.

🏠 2.2%

Rental prices in states with abortion bans declined 2.2% between July 2022 and June 2025 compared to similar markets without restrictions, while vacancies rose 1.1%, according to National Bureau of Economic Research data — a demand shift researchers described as economically meaningful and statistically significant.

▶️ BEST EVER CONFERENCE X

BE GREEDY WHEN OTHERS ARE FEARFUL AND BUY OFFICE

The most hated asset class in CRE may also be its best-kept secret. While institutional capital has fled and CMBS defaults have dominated the news cycle, suburban office has been quietly absorbing space, posting eight consecutive quarters of positive demand — a streak multifamily can no longer match.

Ash Patel made that case at the recent Best Ever Conference, where he laid out the distressed office opportunity with deal-level specificity.

Overall office prices have declined just 17% since 2022 — less than multifamily's 20% drop. But because suburban office goes largely untracked, doom-and-gloom CBD headlines have defined the entire asset class. Meanwhile, multifamily recorded negative absorption in Q4 2025 while 70% of the country's 130 active tower cranes are building more of it.

The next wave of deals is coming. Banks have spent years extending and pretending on toxic office loans, and that era is ending. Ash's advice: get to court-appointed receivers early — they're assigned the moment a bank declares an asset toxic and are among the best sources of off-market deals at distressed pricing.

The retrade is expected: Retrading is standard practice in office — unlike multifamily, where it damages relationships. Ash re-traded a Louisville portfolio from $4.2 million to $3.5 million on the last day of due diligence. The 16-building, 60%-occupied package had sat on the market for two years. Investors are projected to double their money in under four years.

The coworking edge: Membership-based coworking runs like a gym — oversell memberships because not everyone shows up. Ash owns a center in Atlanta where companies pay for memberships their employees never use.

The buy criteria: Target smaller suburban offices near highways or walkable downtowns, staggered lease expirations, and buildings with evidence of active local demand. Cut 20% off your pro forma before committing. Read every lease for termination clauses. If the deal works at 40 cents on the dollar, you can undercut every competing landlord on rent and still win.

The opportunity exists precisely because the competition is thin. Toxic headlines have kept most buyers away, lending has dried up, and the investors still willing to do the work are finding some of the best risk-adjusted deals in CRE — in an asset class Ash believes has already turned the corner.

🙏 Thanks for reading!

Stay in the loop with us! If you received this newsletter from someone else, subscribe here. You can also find us on LinkedIn, Instagram, and YouTube.

Have a Best Ever day!

— Joe Fairless